As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the it distribution & solutions industry, including ePlus (NASDAQ:PLUS) and its peers.

IT Distribution & Solutions will be buoyed by the increasing complexity of IT ecosystems, rising cloud adoption, and demand for cybersecurity solutions. Enterprises are less likely than ever to embark on these complicated journeys solo, and companies in the sector boast expertise and scale in these areas. However, cloud migration also means less need for hardware, which could dent demand for large portions of the product portfolio and hurt margins. Additionally, planning for potentially supply chain disruptions is ongoing, as the COVID-19 pandemic showed how damaging a pause in global trade could be in areas like semiconductor procurement.

The 8 IT distribution & solutions stocks we track reported a very strong Q1. As a group, revenues beat analysts’ consensus estimates by 6.7% while next quarter’s revenue guidance was 9.5% above.

Luckily, IT distribution & solutions stocks have performed well with share prices up 15.5% on average since the latest earnings results.

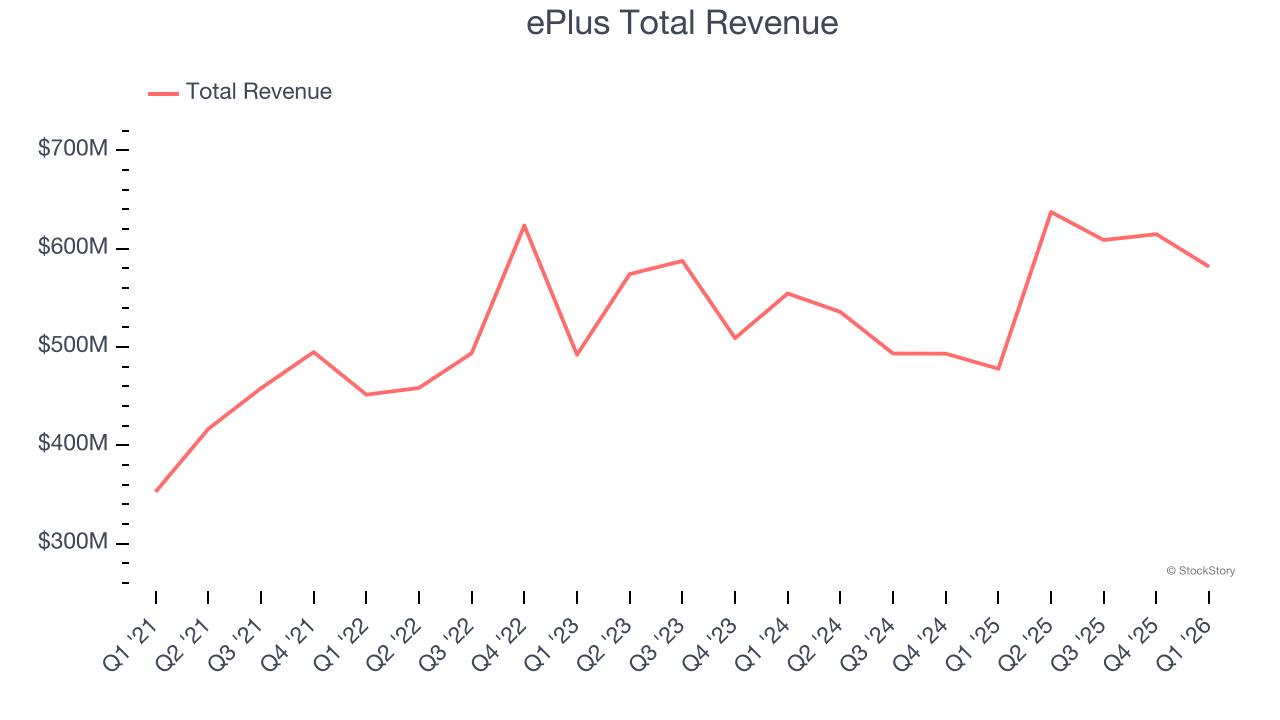

ePlus (NASDAQ:PLUS)

Starting as a financing company in 1990 before evolving into a full-service technology provider, ePlus (NASDAQ:PLUS) provides comprehensive IT solutions, professional services, and financing options to help organizations optimize their technology infrastructure and supply chain processes.

ePlus reported revenues of $581.6 million, up 21.7% year on year. This print exceeded analysts’ expectations by 2.2%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS estimates.

"In the fourth quarter, we achieved double digit growth across both net sales and gross billings, demonstrating expanding market share, and underscoring the durability and resilience of our business, " said Mark Marron, president and CEO of ePlus.

Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 1.2% since reporting and currently trades at $87.55.

Is now the time to buy ePlus? Access our full analysis of the earnings results here, it’s free.

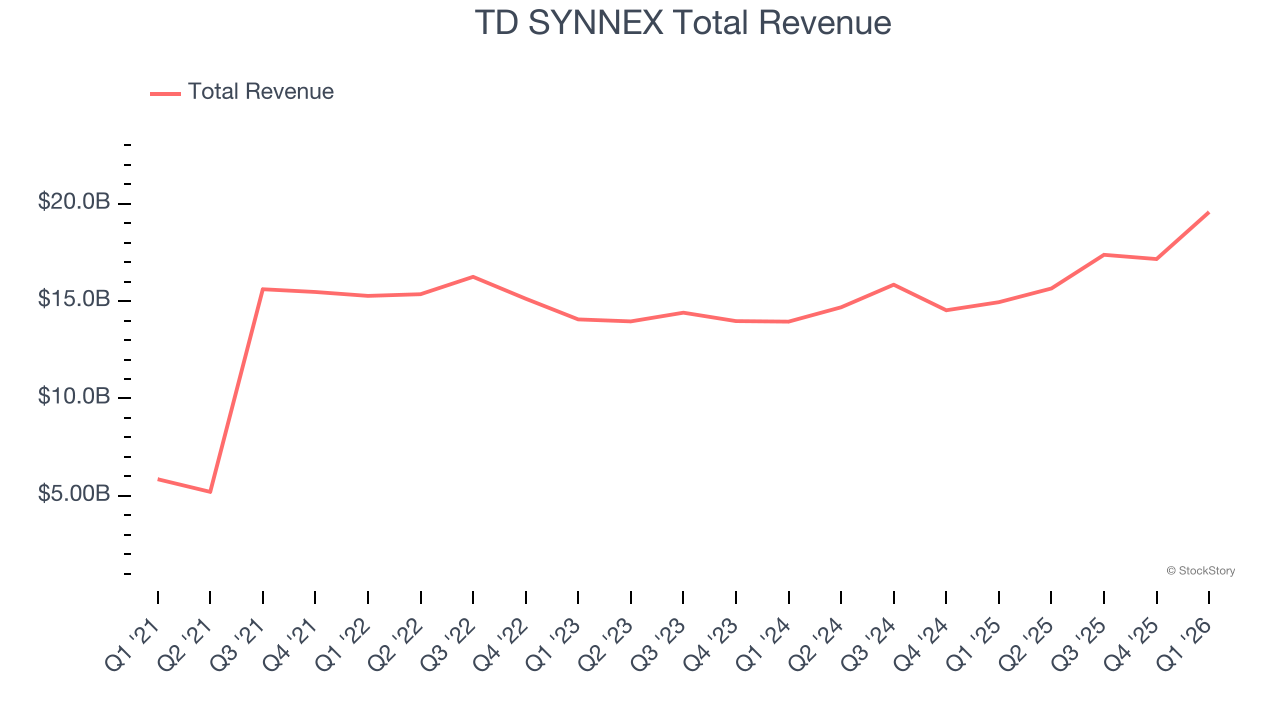

Best Q1: TD SYNNEX (NYSE:SNX)

Serving as the crucial middleman in the technology supply chain, TD SYNNEX (NYSE:SNX) is a global technology distributor that connects thousands of IT manufacturers with resellers, helping businesses access hardware, software, and technology solutions.

TD SYNNEX reported revenues of $19.57 billion, up 31% year on year, outperforming analysts’ expectations by 16.6%. The business had an incredible quarter with a beat of analysts’ EPS estimates.

TD SYNNEX delivered the biggest analyst estimate beat of the whole group. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 9.3% since reporting. It currently trades at $251.45.

Is now the time to buy TD SYNNEX? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Insight Enterprises (NASDAQ:NSIT)

With over 35 years of IT expertise and partnerships with more than 8,000 technology providers, Insight Enterprises (NASDAQ:NSIT) provides end-to-end digital transformation solutions that help businesses modernize their IT infrastructure and maximize the value of technology.

Insight Enterprises reported revenues of $2.13 billion, up 1.2% year on year, exceeding analysts’ expectations by 1.9%. Still, it was a softer quarter as it posted a significant miss of analysts’ EPS estimates.

Insight Enterprises delivered the weakest performance against analyst estimates and slowest revenue growth among its peers. Interestingly, the stock is up 73.6% since the results and currently trades at $119.78.

Read our full analysis of Insight Enterprises’s results here.

Avnet (NASDAQ:AVT)

With a century-long history of adapting to technological evolution, Avnet (NASDAQ:AVT) is a global electronic components distributor that connects manufacturers of semiconductors and other electronic parts with businesses that need these components.

Avnet reported revenues of $7.12 billion, up 33.9% year on year. This number surpassed analysts’ expectations by 10.3%. Overall, it was an incredible quarter as it also put up a solid beat of analysts’ EPS guidance for next quarter estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Avnet achieved the highest guidance raise and fastest revenue growth in the group. The stock is up 10.1% since reporting and currently trades at $86.23.

Read our full, actionable report on Avnet here, it’s free.

ScanSource (NASDAQ:SCSC)

Operating as a crucial link in the technology supply chain since 1992, ScanSource (NASDAQ:SCSC) is a hybrid distributor that connects hardware, software, and cloud services from technology suppliers to resellers and business customers.

ScanSource reported revenues of $766.8 million, up 8.8% year on year. This result beat analysts’ expectations by 6.1%. It was a strong quarter as it also logged a beat of analysts’ EPS estimates.

The stock is up 31.9% since reporting and currently trades at $53.99.

Read our full, actionable report on ScanSource here, it’s free.

Market Update

Over the past year, investors have been forced to repeatedly answer the same question: what is the market’s biggest risk? The answer has changed several times, and each shift has reshaped market leadership.

Late in 2025 and early 2026, artificial intelligence became the market’s primary uncertainty. Investors questioned whether AI would erode software pricing power and weaken competitive moats as AI made it easier to replicate once-differentiated products.

By the spring, technology took a back seat to geopolitics. The U.S. conflict with Iran briefly became the market’s dominant narrative, raising concerns about oil prices, inflation, and global growth. But as energy markets remained orderly and fears of a prolonged supply disruption faded, investors quickly turned their focus back to fundamentals.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.