Since August 2020, the S&P 500 has delivered a total return of 90.8%. But one standout stock has more than doubled the market - over the past five years, AutoZone has surged 237% to $4,001 per share. Its momentum hasn’t stopped as it’s also gained 15.3% in the last six months, beating the S&P by 9.9%.

Is now still a good time to buy AZO? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Is AutoZone a Good Business?

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE:AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

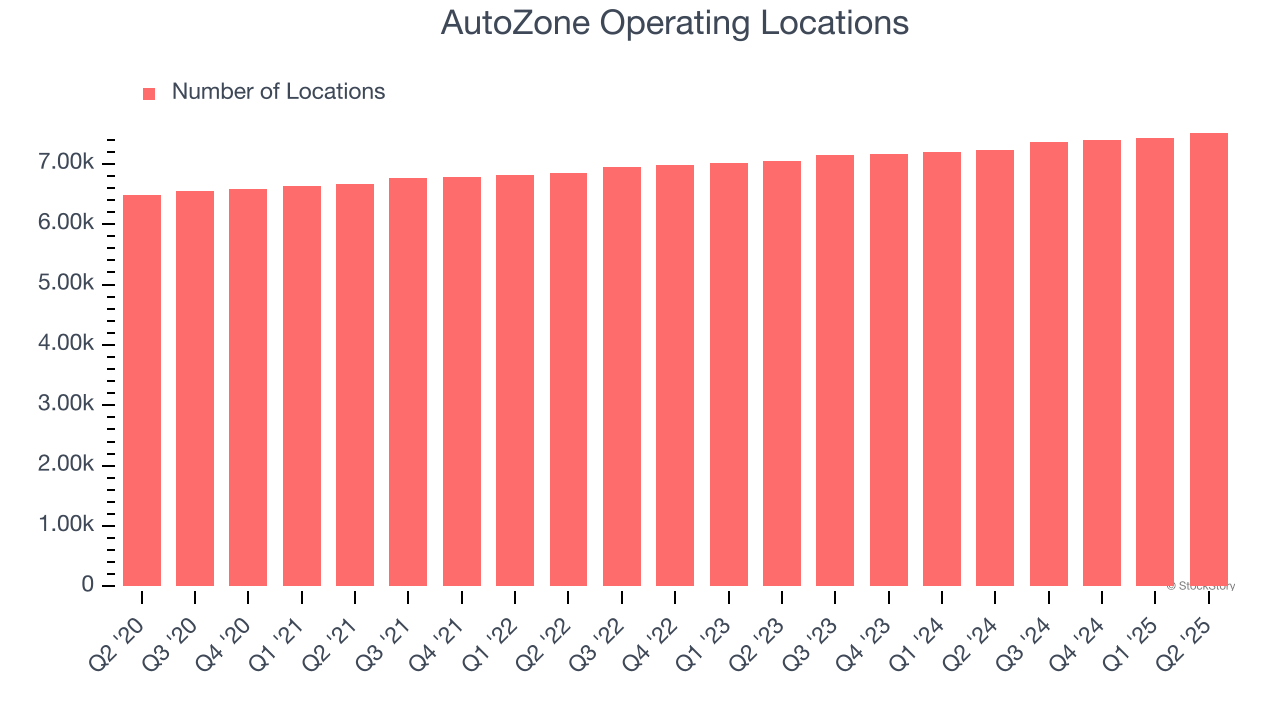

1. New Stores Popping Up Gradually, Supports Growth

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

AutoZone sported 7,516 locations in the latest quarter. Over the last two years, it has opened new stores quickly, averaging 3% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

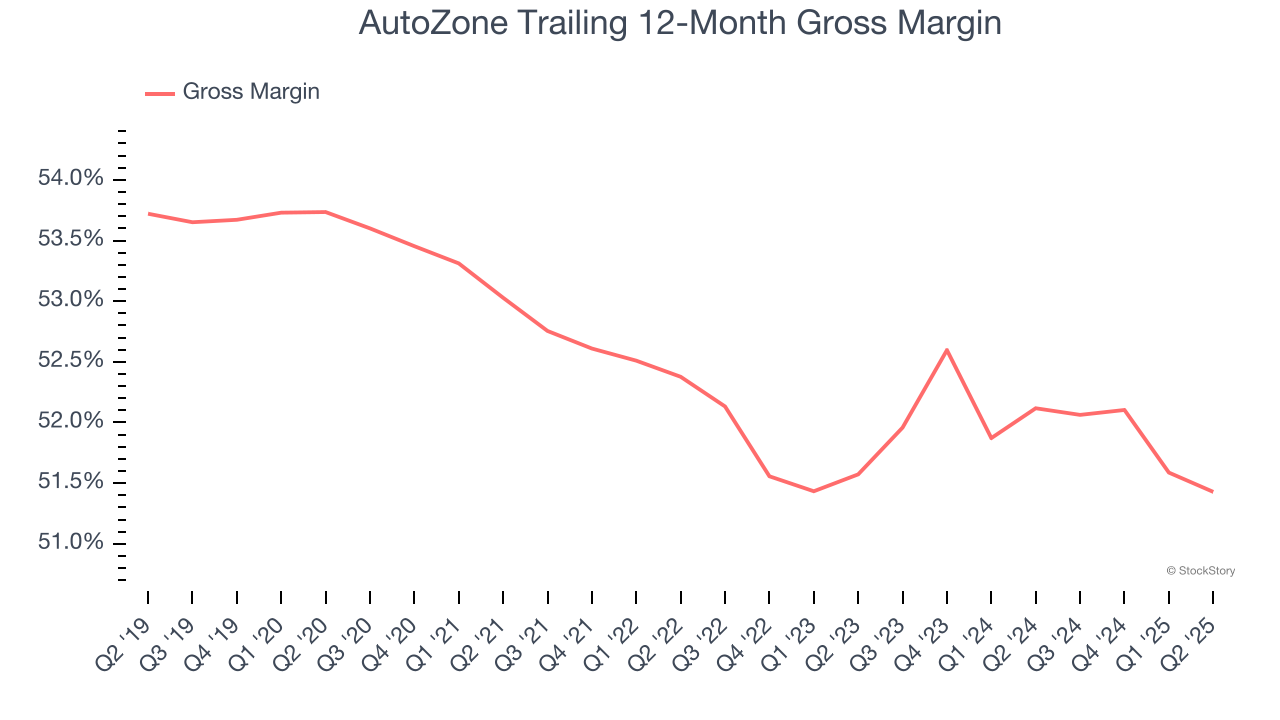

2. Elite Gross Margin Powers Best-In-Class Business Model

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

AutoZone has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent. As you can see below, it averaged an elite 51.8% gross margin over the last two years. That means for every $100 in revenue, only $48.24 went towards paying for inventory, transportation, and distribution.

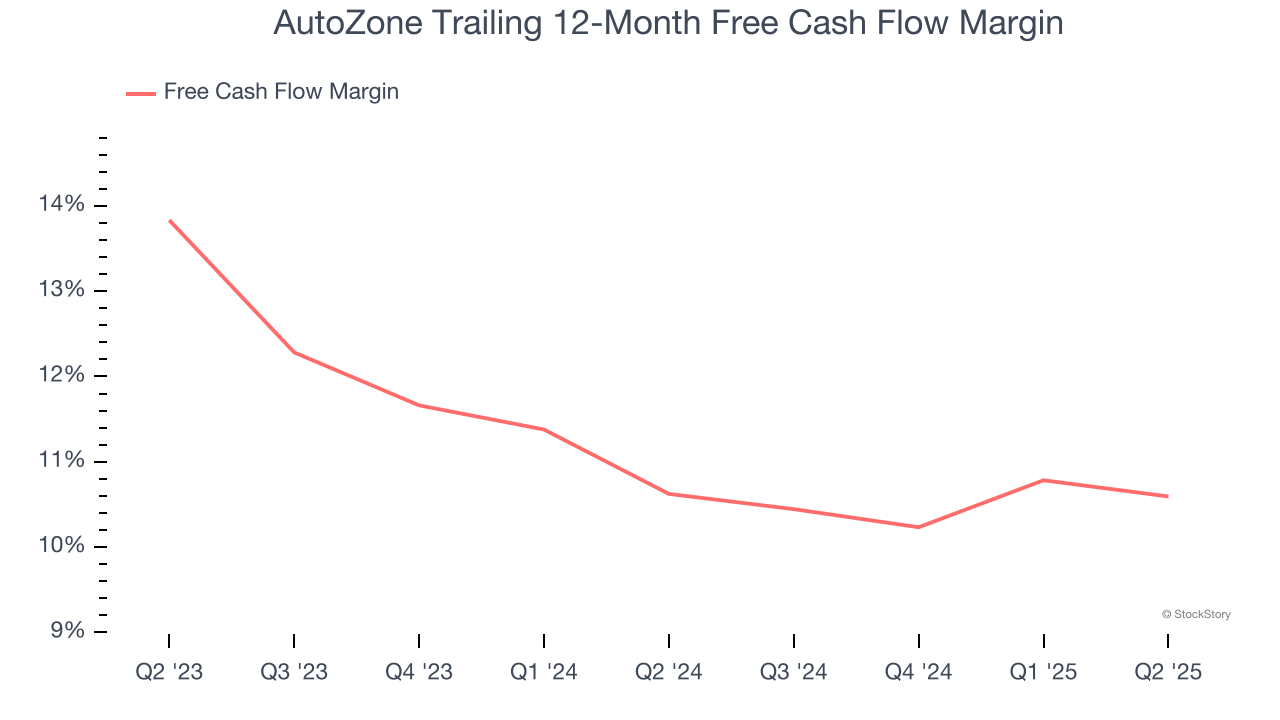

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

AutoZone has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer retail sector, averaging 10.6% over the last two years.

Final Judgment

These are just a few reasons why we're bullish on AutoZone, and with its shares topping the market in recent months, the stock trades at 24.2× forward P/E (or $4,001 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than AutoZone

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.