Visual content marketplace Getty Images (NYSE:GETY) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 2.5% year on year to $234.9 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $949.5 million at the midpoint. Its non-GAAP profit of $0.05 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Getty Images? Find out by accessing our full research report, it’s free.

Getty Images (GETY) Q2 CY2025 Highlights:

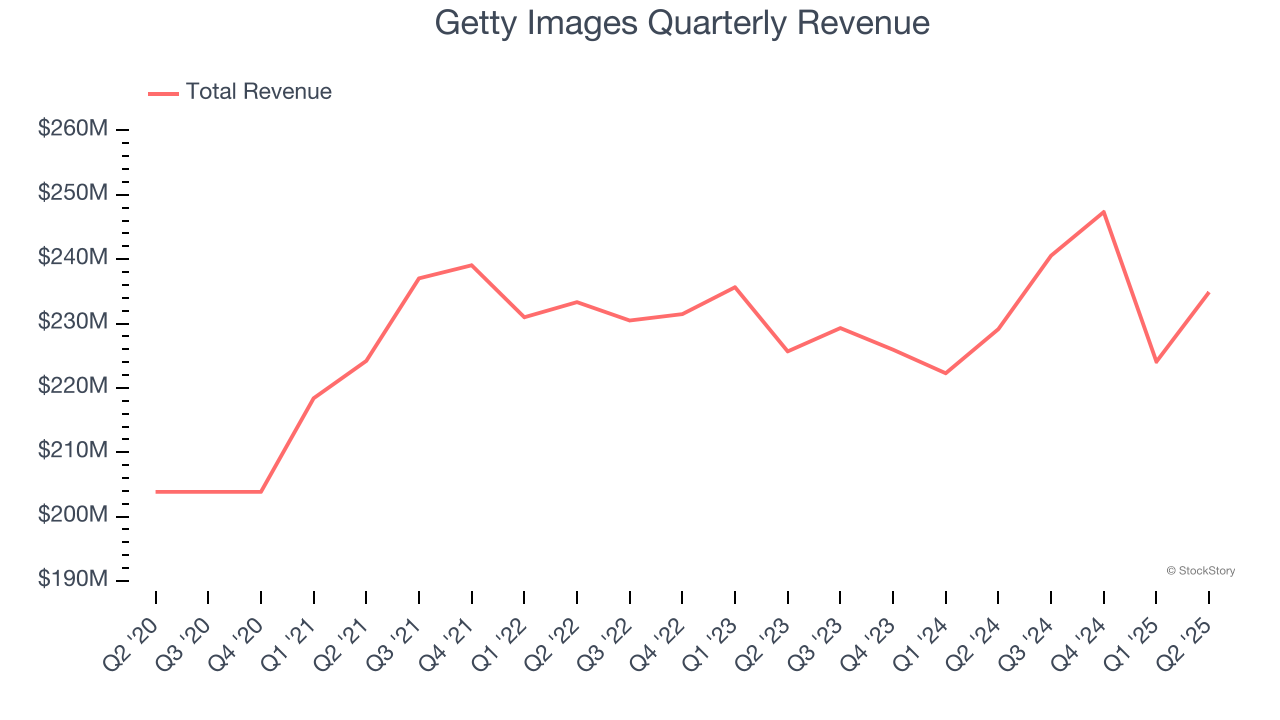

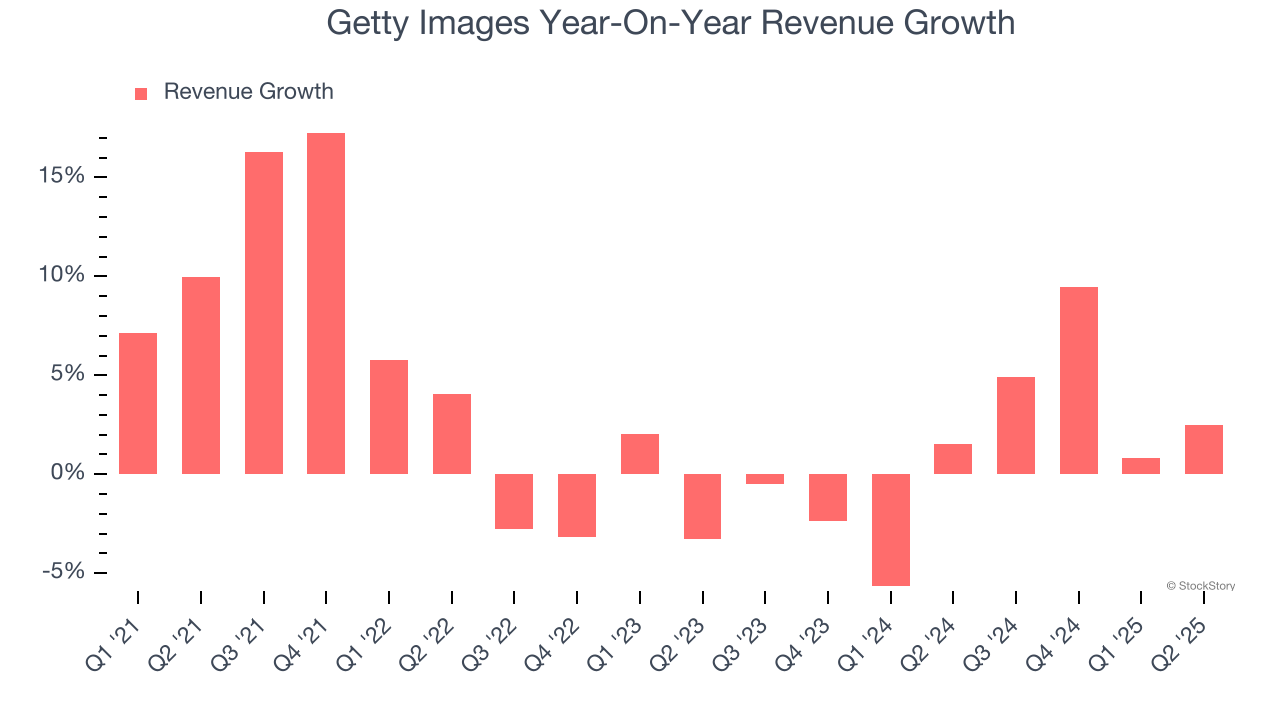

- Revenue: $234.9 million vs analyst estimates of $235.8 million (2.5% year-on-year growth, in line)

- Adjusted EPS: $0.05 vs analyst estimates of $0.01 (significant beat)

- Adjusted EBITDA: $67.97 million vs analyst estimates of $71.29 million (28.9% margin, 4.6% miss)

- The company reconfirmed its revenue guidance for the full year of $949.5 million at the midpoint

- EBITDA guidance for the full year is $287 million at the midpoint, in line with analyst expectations

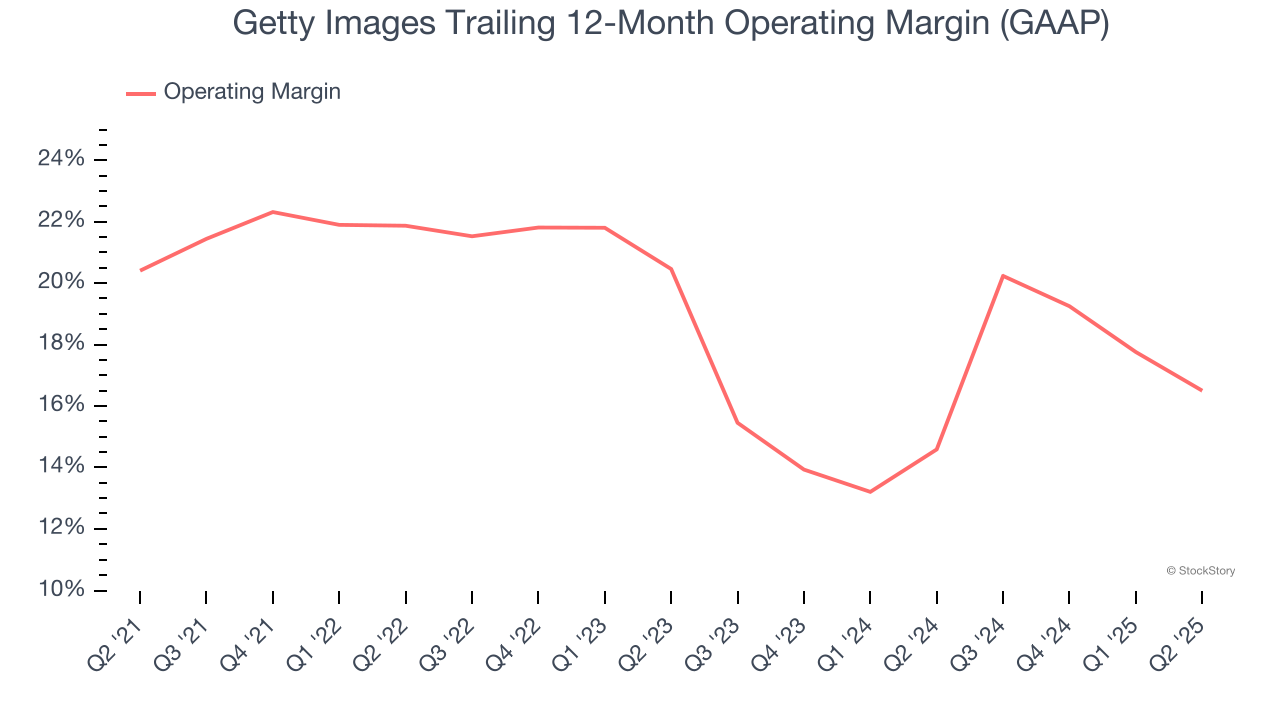

- Operating Margin: 15.1%, down from 20.3% in the same quarter last year

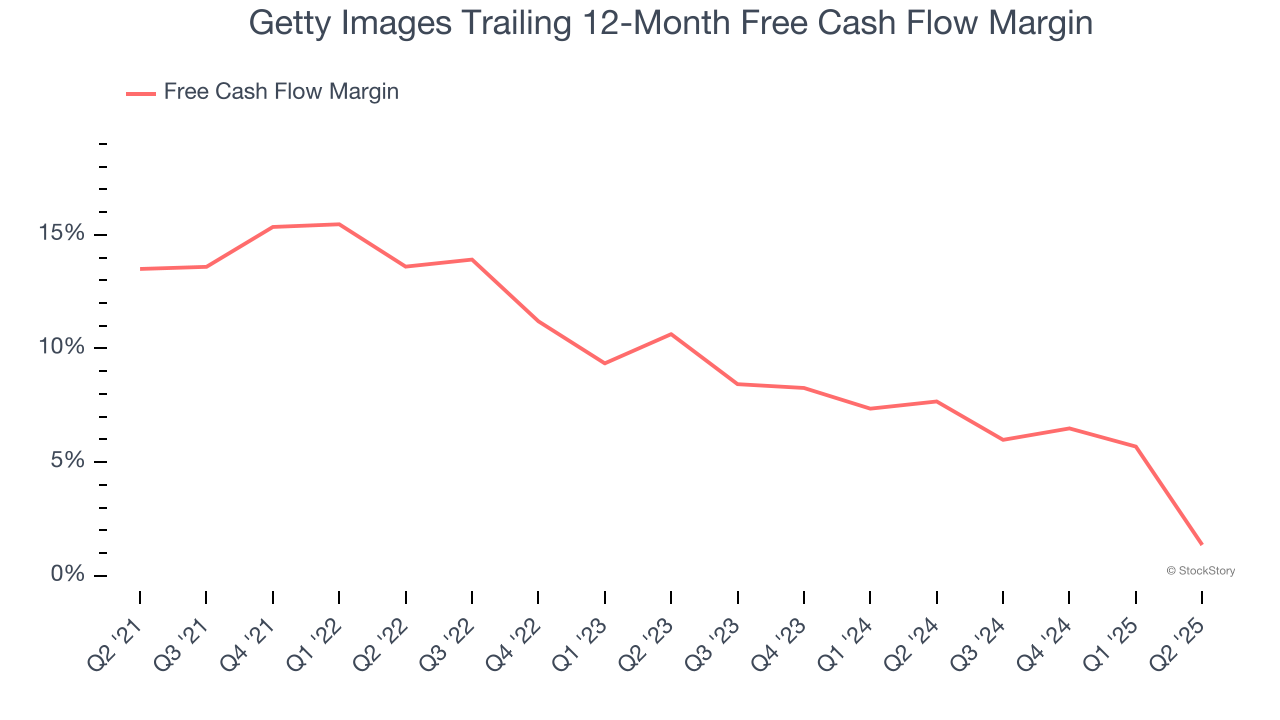

- Free Cash Flow was -$9.57 million, down from $31.06 million in the same quarter last year

- Market Capitalization: $701 million

“We delivered solid growth in the second quarter, driven by continued momentum in our subscription business and strong demand for our content and services with acceleration across Corporate, and a return to growth in Media," said Craig Peters, Chief Executive Officer at Getty Images.

Company Overview

With a vast library of over 562 million visual assets documenting everything from breaking news to iconic historical moments, Getty Images (NYSE:GETY) is a global visual content marketplace that licenses photos, videos, illustrations, and music to businesses, media outlets, and creative professionals.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $946.8 million in revenue over the past 12 months, Getty Images is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels.

As you can see below, Getty Images’s 2.4% annualized revenue growth over the last five years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Getty Images’s recent performance shows its demand has slowed as its annualized revenue growth of 1.3% over the last two years was below its five-year trend.

This quarter, Getty Images grew its revenue by 2.5% year on year, and its $234.9 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not catalyze better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Getty Images has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 18.8%.

Analyzing the trend in its profitability, Getty Images’s operating margin decreased by 3.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q2, Getty Images generated an operating margin profit margin of 15.1%, down 5.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Getty Images has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.3% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that Getty Images’s margin dropped by 12.1 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Getty Images burned through $9.57 million of cash in Q2, equivalent to a negative 4.1% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

Key Takeaways from Getty Images’s Q2 Results

We were impressed by how significantly Getty Images blew past analysts’ EPS expectations this quarter. On the other hand, its revenue was in line. Overall, we think this was a decent quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 5.2% to $1.63 immediately following the results.

Is Getty Images an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.